This article first appeared in the March 2024 issue of the GreenMoney Journal and is reprinted here with permission. Learn more at greenmoney.com.

Female business owners face specific and unique challenges. Kersy Azocar, President and CEO of Greenline Access Capital shares her personal experience with applying for a business loan and the barriers that she encountered.

“When I applied for my first loan, prior to reviewing any of my information or asking any questions, the banking specialist immediately mentioned that I may need my husband to cosign the loan. When I told the specialist that I was in the financial industry and that I did not need my husband’s help to qualify for financing, he would not budge. I did not apply at that bank – they did not deserve my business. Implicit Bias and Barriers in financing such as this are a common reality for women all over the world.”

For many years, women have had a more difficult time accessing capital, and typically, have had a higher cost of capital. Because traditional services have failed to reach many of them, women business owners need alternative channels to access capital, offering more support and opportunities.

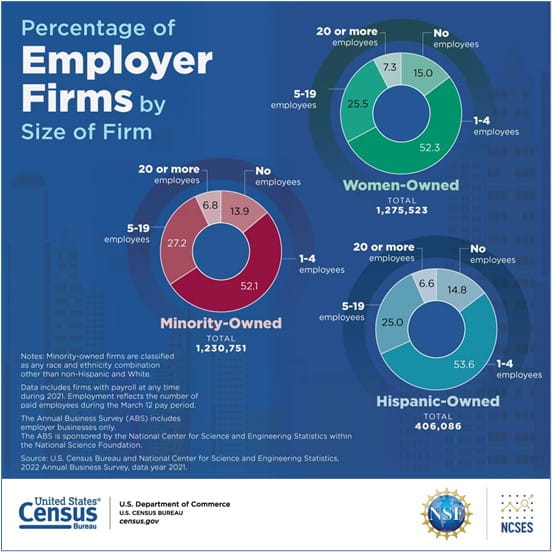

A recent, post-pandemic study by the U.S. Department of Commerce demonstrated what we already know: that female-led businesses play an important role in the economy as shown in the chart below. There are over 1.2 million women owned business, a third of which hire five or more employees.

Women owned businesses meet community needs

Even with widespread pandemic-induced layoffs, women started businesses at a higher rate than men. Increased flexibility in schedules especially for women with school-aged children motivated more women to start their own businesses. They often brought that flexibility to their employees through work-from-home opportunities and creative hybrid work schedules.

A Gusto News study found that women were more likely to open businesses with a community focus and these were often in the personal services, healthcare, education and nonprofit fields, proving that, when they thrive, the whole community benefits.

Unique challenges faced by female entrepreneurs

In the U.S., research has shown that women face greater capital constraints than men. Compared to men, female entrepreneurs – especially those from low-to-moderate income communities – often do not have a long track record of business ownership, have little to no pre-existing wealth, lack home equity and collateral, and often have poor credit history. Due to these factors, female entrepreneurs are often disqualified from traditional financing. This means that for many, self-financing or costly forms of capital with higher interest rates are their only option.

Those are not the only barriers for female entrepreneurs. Despite significant growth potential, there is an underlying perception that it is difficult to get traditional financing, which leads to an unwillingness to go through seemingly tedious loan search and application processes that take up precious time and are costly. Additionally, female and minority-owned firms are disproportionately denied when they need and apply for additional credit, and depending on location, there may not be any other firms offering the type of capital these entrepreneurs need.

The United Nations identified the need to invest in women in two of its Sustainable Development Goals. Goal 5 (gender equality) and Goal 8 (decent work and economic growth) both pay particular attention to creating opportunity for female entrepreneurs. There is immense opportunity for sustainable investors and capital providers to meet the needs of women business owners who are in need of financing to support and grow their businesses.

How capital providers can help

There are a number of ways capital providers can meet the needs of female entrepreneurs when it comes to financing.

First, capital providers need to be cognizant of the fact that there is a gender barrier that prevents many women business owners from accessing traditional financing. Providers can and should actively work to reduce and eliminate these barriers.

A good place to start is to analyze the lender’s history of ‘who applies for’ versus ‘who receives’ financing and the reasons for denial. Additionally, capital providers can proactively create products that are a good fit for female entrepreneurs and allow for outside-the-box thinking when it comes to risk and return.

A recent partnership between Greenline Access Capital, a mission-driven nonprofit financial institution that works to address the continued and persistent gap in access to capital for financially underserved entrepreneurs in Philadelphia, PA, and Everence Financial®, a faith-based financial services company, seeks to bridge this gap.

Since 2021, Greenline has served more than 250 people and has helped 48 clients connect with $5.3 million in grants and loans, including 23 loans from Greenline’s own funds. Of these loans, 48% were made to women-owned businesses. By collaborating with Everence, Greenline is able to connect mission-driven funds with underserved businesses, many of which are women-owned. By combining the provision of capital, customized technical assistance and training focused on entrepreneurial and financial success, these types of organizations are helping bridge the gap in serving communities and individuals often excluded.

By creating long-term relationships with organizations like Greenline Access Capital, capital providers can support impact at scale by increasing efficiency and productivity for all parties. These partnerships can cross public, private and non-profit capital sources and can function locally, regionally or across the country. Though more work is required, especially at the beginning of the relationship, in the long run these partnerships will pay off for both capital providers, alternative lenders and underserved communities.

Family need meets business opportunity Gladis Avila, Venbisustore owner (center), with Greenline Access Capital staff, Gleidys Arias, Program Manager (left) and Kersy Azocar, President and CEO, (right).

Gladis met Greenline Access through one of its partners, The Welcoming Center and became a client. Through their help she received a microloan and a matching grant from the City of Philadelphia which helped her purchase inventory and equipment so that she would be ready for the holiday season and increase her sales. Her plans for the future include opening a store in Philadelphia, Pa. Greenline is excited to help Gladis connect with mission-aligned organizations such as Everence for additional funding when she needs it.

How investors can help

It is no surprise that impact investors are particularly interested in supporting these women-owned small businesses that are important drivers of the economy. Through community development investing, investors can support mission-driven alternative lenders, like Greenline, that focus on connecting female entrepreneurs with capital. These institutions are nimble and innovative in reaching women business owners in a way traditional lenders often are not.

A simple way for individuals or institutions to support women-owned businesses in underserved and underrepresented communities is to identify investment products that channel all or a portion of assets to community development investing. This can include mutual funds – like Praxis Mutual Funds, a fund family of Everence – that invest a portion of each fund in high-social impact community investments through qualified partners.

Community lending specialists, like Calvert Impact or Capital Impact Partners, offer products for both institutional and retail investors. And many community development banks and credit unions offer ways to channel financing to benefit specific communities. To learn more, visit: praxismutualfunds.com, ussif.org/communityinvesting, or inclusiv.org.

Community development investing can help move us closer to a more equitable and inclusive economy by closing the gender gap in business ownership – and we all have an important role to play.

Authors:

Stella Tai, Stewardship Investing Impact and Analysis Manager, Praxis Mutual Funds

Kersy Azocar, President and CEO of Greenline Access Capital